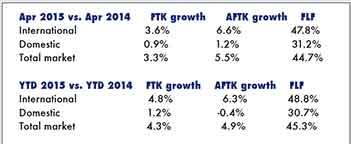

The International Air Transport Association (IATA) has released data for global air freight markets showing a 3.3 per cent increase in cargo volumes (freight tonne kilometres or FTKs) in April 2015 compared to April 2014.

However, there has been no growth in aggregated global cargo volumes since late last year.

At a regional level, only Asia-Pacific and Middle Eastern airlines reported growth in April. North American carriers reported essentially flat demand, while Europe, Latin America and Africa all reported declines when compared to 2014.

April data also revealed a slowdown from the growth for the first quarter of 2015 at an average 5.3 per cent, in line with a recent weakening in world trade growth. Despite a cyclical pick-up in the global economy, acceleration in trade and air freight demand is seen as unlikely in the near term as business confidence and export orders are flat or declining.

“After a volatile start to 2015, the market is settling down, and it is clear that momentum in air freight growth is being lost. First there is the structural challenge of world trade no longer expanding at a faster rate than domestic production. Layered on top of that trend we now see a weakening of economic indicators in the crucial air cargo markets of Asia-Pacific and Europe,” said Tony Tyler, IATA’s director general and ceo.

“These factors point toward a need to kick-start trade by reversing protectionist trade measures. Implementing the Bali Trade Facilitation Agreement would be a good start, as well as commitments to help facilitate trade in emerging markets,” said Tyler.

Also of note was the significant capacity increase of 5.5 per cent in April 2015, driving the load factor down to its lowest for the past 12 months.

Regional analysis in detail Asia-Pacific carriers reported demand growth of 4.5 per cent in April compared to April 2014, below a capacity expansion of seven per cent. Current trade volumes for emerging Asia markets are down 10 per cent, and the region has been affected by a slowdown in exports to Europe.

European carriers saw demand decline by 0.3 per cent in April, compared to a year ago while capacity grew by five per cent. Recent improvements in European business confidence have yet to be reflected in air freight volumes. A firming-up of oil prices and the Euro has meant that positive momentum from the European Central Bank stimulus has faltered.

North American airlines reported demand growth of 0.1 per cent year-on-year while capacity was cut by 1.6 per cent. A disappointing economic performance in the first quarter is expected to improve in the coming months, with the likely impact of falling oil prices and the end of the West Coast port strikes.

Middle Eastern carriers saw demand grow by 14.1 per cent on the back of increased trade within the region, along with network and capacity expansion. Capacity grew 18.5 per cent. Latin American airlines reported a fall of 6.8 per cent in demand, while capacity grew by seven per cent. Month-on-month results for carriers in the region indicate that recent declines may have come to an end. The hope is that general increases in regional trade activity start to be reflected in stronger air freight demand.

African airlines experienced a 0.2 per cent decline in demand and a 2.2 per cent decrease in capacity. The region still appears to be affected by the under-performance of the Nigerian and South African economies.

Bottom Line “After a brief optimistic period, the global outlook for cargo shows that once again the business is stagnating. But the good news is that with digital processes, new standards for pharmaceutical handling, and a focus on reducing end-to-end shipment times the air cargo industry is well-placed to stage a recovery,” said Tyler.

By Andrew Hudson, Partner, Gadens Melbourne. E: This email address is being protected from spambots. You need JavaScript enabled to view it.

Impending changes to Australia’s National Cargo Security Program (NCSP) relating to US-bound air cargo will require both the Office of Transport Security (OTS) of the Department of Infrastructure and Regional Development and affected industry to effect significant changes.

As a director of the Export Council of Australia (ECA) I have attended recent meetings of the Cargo Working Group (CWG) convened by the OTS. Clearly, many members of the ECA will be affected by these changes as will others in industry.

As many would be aware, Australia has not been subject to strict compliance with the requirement of the US TSA that all US-bound air cargo be examined at “piece level”. However that situation is shortly to expire after the TSA undertook an audit of our NCSP and recommended that 100 per cent of US-bound air cargo be examined at ‘piece level’. While the OTS continues to negotiate with the TSA to resolve the issue as soon as possible, the TSA has extended recognition until at least 31 July 2015.

At the most recent meeting of the CWG, the OTS revealed its proposed program to meet the requirements of the TSA for such ‘piece level examination’. This would require an exporter to either come within a ‘Known Consignor’ (KC) scheme or to ensure that its goods were subject to piece level examination of cargo, otherwise such cargo would not be able to be loaded. The OTS advised the CWG that the proposal was acceptable to the TSA and that it had secured Government approval to proceed with policy design and implementation. However, that does not extend to the provision of financial assistance to assist industry in managing the changes.

In the interests of providing ‘highlights’, some preliminary information is set out below:

• The new program will apply to air cargo touching on the US, whether unloaded there, or being transited through the US to be on- shipped to third countries.

• While the new program will apply to the US, the measures will be aligned with ICAO standards and meet the requirements of other areas such as the EU. The ideal would be for there to be uniform standards for all air cargo and the OTS would not object to exporters applying the program to exports to other countries.

• The aim will be for freight from KCs to be accepted without further screening by airlines as occurs elsewhere in the world. That is still subject to discussions with CTOs

• In common with Customs’ Trusted Trader Programme’ (TTP) the new scheme will address cargo security. However, the TTP does consider security in a wider context to include the entire supply chain. The OTS is working with Customs and other government agencies so that security measures in the various government ‘trusted’ programs include similar requirements so far as possible.

• The ‘regular customer’ requirements will not satisfy the requirements of the TSA and those ‘regular customers’ exporting by air to the US will need to make other arrangements.

• Membership of the KC scheme will be voluntary and subject to OTS validation and ongoing compliance oversight. OTS has indicated that the scheme will be designed to allow industry flexibility in meeting the security requirements while still satisfying the requirements of the TSA (and other jurisdictions).

• Piece level examination for those that are not KCs will be addressed in an Enhanced Air Cargo Examination (EACE) Notice to be issued by the OTS. That will set out the approved standards and methods of examination (which may include x–ray, explosive trace detection and physical examination).

Businesses providing the examination will be accredited. The current ACE notice will be amended so that cargo examined under the EACE Notice will not require additional examination at the CTO.

• Timing has yet to be finalised and subject to negotiation with the TSA. The EACE will be available to the express freight industry by 1 July 2015 and to off–site freight forwarders by 1 March 2016. The KC scheme should be open by 1 July 2016. The date for full adoption of 100 per cent piece level examination through our program has not been set although the TSA will want a firm set date that could be as early as 31 December 2016.

Clearly, there is much detail to be developed and the OTS has now embarked on an extensive process of engagement with industry including providing information as well as mapping the export process to better understand that process to allow the development of an effective program.

We do live in interesting times in the supply chain. This is taking place at the same time as Australia seeks to implement the WTO Trade Facilitation Agreement and pursue its own de – regulation agenda seeking to reduce the regulatory burden on business. However the security imperative from the TSA will always trump all those other considerations. Hopefully, Government can soften the blow by changing its position on support to business by providing financial and non-financial assistance. All businesses, especially SME exporters would be very grateful!

Businesses seeking more information about the arrangements can contact OTS via e-mail at : This email address is being protected from spambots. You need JavaScript enabled to view it. or by calling: 1800 007 024

COMPANIES that intend to use disruptive technologies will have to step outside their comfort zones and take some risks in order to reap the potential rewards, according to Australian business consultancy UXC.

UXC says success depends on minimising those risks where possible by taking a staged and carefully considered approach and working with a technology partner that understands their business, its challenges and its goals.

Cris Nicolli, managing director UXC said while disruptive IT projects carry a certain amount of risk, it is possible to reduce this risk by following eight key steps.

1. Create the business case. There are three main disruptive technology costs: Financial, time and perception and organisations must understand not all projects will run smoothly or achieve the planned outcomes.

The business must clearly articulate and analyse issues including costs and develop a strong business case for investment before taking the next step.

Innovation and disruption are unlikely to be valuable unless they are properly resourced and strategically targeted.

2. Understand and agree on the business requirements up front. Most firms implement technology in order to fulfil customer and organisational needs more effectively.

They therefore must clearly articulate the business requirements/outcomes sought before deciding on the technology to be implemented.

3. Engage key stakeholders.To bring stakeholders including employees and end users on board, they must understand how the project fits the broader business goals.

To make them fully engaged and enthusiastic about it, there needs to be clear, consistent ongoing communication including updates from the executive leadership and the project team to the rest of the stakeholders.

4. Secure executive sponsorship.Executive support is an indication that the entire company is committed to making the technology implementation work.

Without it, project teams can lose sight of the organisation’s strategic goals and failure becomes more likely.

5. Choose the right technology.While disruptive technology may look attractive, it is not necessarily the right choice. On the other hand, if a disruptive technology is the one most likely to deliver business benefits then organisations should not be dissuaded by the potential risks.

As long as the organisation has done appropriate due diligence, has a strong risk management regime in place and knows it is making the right solution, it should be well placed for success.

Choosing the right technology requires businesses to review a variety of parameters including: Depth of functionality; industry-specific features; ease of support; future development path; flexibility to adapt to the changing business model; integration with existing/future systems and scalability.

6. Future-proof the decision.By selecting a technology that maps closely to the current and future state of the business, risks are reduced. It also often is advisable to choose a solution that does not require a large amount of customisation, as this can add to ongoing running costs and future upgrade complexity. Choosing a technology that offers maximum functionality and scalability at the outset will reduce the need for constant upgrades over time. Effective organisational change management also plays a role in future-proofing the decision. 7. Demand post-implementation support.An implementation project does not end once the technology goes live. It is vital to have effective and well-resourced support in place. This will help ensure the system is fully operational, delivering value to the business and improving the productivity of those using it. 8. Implement effective governance. Corporate governance is essential for an organisation’s ongoing success and this extends to technology implementations. The greater the level of governance and scrutiny, the lower the risk of a project not succeeding. Effective governance includes the oversight of the project itself, from high level aims to detailed tactics, to ensure the project stays on track. The level and intensity of governance should be scaled to match the level of complexity of a project and the size of its investment.

DESMOND (Des) Vertannes (left) has spent more than 40 years working in air cargo. Those who know him best – and he is widely known and hugely respected in air cargo – know he strives to improve the industry. His career has included time at Air Canada, Etihad Airways and most recently, four years as head of cargo at the International Air Transport Association (IATA). He currently works as a strategic adviser at SmartKargo.

How did you come to work in air cargo? Des Vertannes: No one plans to enter the air cargo business. About 99 per cent of us fall into it by accident and I was one of those. I originally wanted to become a teacher, but as the oldest of 10 children, my father thought that earning money ‘sooner’ made more sense. I started with British European Airways (BEA) in its air cargo unit at London Heathrow, helping fill the bellies of their Tridents, BAC-111s, Viscounts and dedicated Vanguard freighters called Merchantmen – planes barely recognised today.

Let’s start with a broad view: what are the three biggest challenges air cargo faces? Security, barriers to open trade in goods and the rise in eCommerce. The first two are challenges or threats, and the last is both a threat and a remarkable opportunity.

1. The focus on security has been with us for decades, but became much sharper after 9/11 and security initiatives from government and others are ubiquitous now. What we need is a more nuanced and collaborative approach.

2. There’s not much that needs saying about tariffs and other barriers to trade in goods – most of us agree that increasing government protectionism harms world trade and hence our industry.

3. The dramatic growth of eCommerce is driven by evolving consumer behaviour. People like to buy things on line because it’s convenient, making price and feature comparisons are easy - and above all it’s fast. Universally, middle-class families are busy, and internet shopping saves time. In order to meet this growing – and to me irreversible – trend, air cargo people need to learn to adapt more quickly. Historically, we’ve not been good at change, and especially not at fast change.

How can advancing information technology help address these three challenges? I became interested in cargo IT to facilitate the fast and efficient transfer of information to all who use it. Whoever needs data should get data.

But that doesn’t happen much today. There are all kinds of blockages, some for selfish reasons that are not clearly thought out – “it’s mine” is something a three-year-old says. And even when key information does transfer between parties, it can become distorted. Sometimes governments are to blame, but often it’s the industry or the people we’ve hired to design our software and systems. Traditional air cargo IT providers see a wholesale solution, that is, airport to airport, rather than a more comprehensive and essential retail solution, from shipper to consignee. Integrators like FedEx and DHL figured this out decades ago, and it’s no wonder they’ve prospered ever since. Air cargo needs to understand this.

Another thing I learned is that developing a system in house is in most cases not the right move. Time and time again, I have seen the “make or buy” decision go in the wrong direction. The temptation to develop internally can be prompted by the best of intentions - but cost over-runs, missed deadlines and what actually is delivered can be a huge disappointment. Moreover, in my experience airlines often are delivered a system that is behind the curve in technology. It makes much more sense to contract with a proven system built for the future, not the past.

You’re a strong advocate of getting rid of paper. What’s wrong with paper? Air cargo providers move goods from point A to point B, but traditionally that also involves a whole bunch of paperwork to support each shipment. So we move the paper, and sometimes we lose the paper. And when we lose the paper, we can’t deliver the box. It’s that simple.

If we want to see what paperless can do, we need only ask our colleagues on the passenger side. The rise of e-tickets transformed distribution and lowered costs.

You’ve spoken publicly about culture change. What do you mean? It seems nearly everyone wants someone else to do the work, to make change happen.

We need leadership and we need people to take ownership. That’s the culture change. Air cargo is stuck in the old ways that no longer work.

Relationships with others in the cargo chain need to change, too. Airlines used to treat freight forwarders very paternalistically – the carriers expected forwarders to do what they were told to do. But that’s no way to treat partners, and the industry is evolving to a B2B model and procedures that treat others in the cargo chain as peers, not subordinates.

Some carriers still treat cargo as a sideline. What can be done to change that? IATA campaigned among its member airlines a few years ago to raise awareness of the value of cargo. There were three audiences: Airline ceos, government agencies (for airport investments) and the marketplace, especially investors. Among IATA member carriers, cargo averages 12 per cent of revenue, three times the average value of first class passenger business (four per cent). Yet look at all the investment in the first class product: Limousines to and from the airport, departure and arrival lounges, huge seats that turn to beds, the latest in-flight entertainment, spectacular food and wine and more. Last year, the cargo share had dropped to nine per cent and first class was still four per cent. Airlines simply do not invest what they should in cargo. Part of the reason is ‘the vicious cycle’: Low cargo revenue leads to low or no investment in IT and other items, which in turn produces disappointing revenues. It’s time to create a virtuous cycle! I also think that longer-range wide body aircraft, with ample bellies, will start to change the focus. The world is shrinking and anywhere is now one stop away. Cargo revenue will help justify the decision to buy and fly these big, long-flying planes. We’re already seeing evidence of that in North American and other carriers.

What’s your view on airlines trying to build their own cargo system? An analogy works well here: Pretend I’m pretty good with tools, and I could, with some help, build an automobile. It would run, it might even go fast enough to use on the motorway. But it would not be as good as the car I could buy from a global brand. Automobile makers invest billions in the best technology, the best safety, the best energy efficiency and styling. It works that way in cargo IT, too. Yes, you could build your own, but why wouldn’t you take products from someone who’s already done it - and done it to a very high standard. Lots of airlines have opted to build a system themselves and after millions of dollars and years of waiting have had little to show for it – and in some cases nothing.

Finally, what are the winning systems/services/products that you have access to now? I’ve advocated end-to-end solutions for years. And being 100 per cent in the cloud gives companies enormous power, for example, in making the same information visible at the same time to everyone who needs to know. SmartKargo, for example, was designed around every partner in the cargo chain, not just the carriers; Air cargo is an ecosystem, and every partner needs to be linked. That means customising tools to suit the needs of the individual, making sure systems can adapt to the particular needs of an airline.

GLOBAL freight-only giant carrier FedEx has stepped into the growing row between three US carriers and Gulf airlines Emirates, Qatar Air and Etihad (and their respective governments) and has pointed out that the three ‘foreigners’ not only carry a tidy proportion of US exports that travel by air, FedEx itself has a stake in maintaining the status quo because of its flights to and investments in the gulf region.

FedEx – which flies a fleet of 660 cargo planes across the world - has warned the US White House that any action it takes to limit foreign competitors will be seen by many as “the cold wind of US protectionism.”

And, with a major hub expansion under way in Dubai, it has stated bluntly that “we (FedEx) would potentially be subject to the greatest harm” if the United States moved against its gulf competitors.

Two other US companies with stakes in the game, United Parcel Service (UPS) and plane maker Boeing, have been coy about the case until now, but both know any changes to bilaterals would impact them severely.

While Dubai-based Emirates SkyCargo alone carries about 1000 tonnes of outbound freight a week from the USA, until now the row has been focused on the cabins, with Delta, United and American airlines claiming that the three Gulf carriers are able to offer ‘cheap’ fares to US international travellers thanks to government subsidies totalling about US$42 billion given over many years.

The three Gulf airlines have since asked for time to counter these allegations, but say any funds/benefits from their governments are only offered to them on commercial terms.

In the meantime, The US airlines had hoped the gulf carriers would freeze flights to the United States while talks between the various governments were under way, but both Qatar and Emirates continue to boost their US networks, with no halt planned. In terms of freight, Emirates SkyCargo in particular, with strong freight ties to the US, offers a compelling network of international destinations for US exporters. SkyCargo – (2014-15 financial year revenues US$3.4 billion) already serves 10 US ports using freighters and belly hold space and recently announced plans to add Orlando.

The entry of FedEx – opening the dispute to include its impact on international trade – is long overdue.

Many overseas commentators have been bemused that the Obama administration has not already dismissed the three US carriers’ complaints out of hand. Considering that only Delta and United even fly to the Gulf (and only once a day each), the vast majority of passengers and air cargo that is routed to or via Dubai (Emirates’ hub), Abu Dhabi (Etihad’s) and Doha (Qatar Air’s) have no alternative flight options other than often-longer and potentially more-expensive flights via partner carriers in Europe and Asia or Asia-Pacific.

These airline partnerships – oneworld, Star Alliance and SkyTeam – currently have more than 60 international carrier members, fly to more than 500 countries and carried more than 1.6 billion passengers last year. Some of the partner airlines including oneworld’s IAG (it has Qatar Air as its biggest shareholder) have told their US partners that they can not support a challenge to the Gulf carriers.

At home, however, FedEx already faces some carrier opposition to its stance. In a 2012 case, FedEx argued that the US government should establish a level playing field for cargo and prohibit state-owned foreign enterprises from cross-subsidising FedEx’s competitors. That case may come back to bite the freight carrier.

In the meantime, FedEx managing director has written an 11-page formal filing to the US Department of Transportation that argues against any US changes to Open Skies.

The cargo company says US airlines commonly use Open Skies agreements to build their international networks and that they eliminate competitors by working with foreign airlines. “In this case, we believe consumers (who benefit from lower fares) should be allowed to be the winners,” Sparks wrote.

Open Skies agreements with more than 100 nations allow equal access to one another’s airports without interference from the respective national governments. FedEx argues that access to the three mega-airports that have been built in Qatar, Dubai and Abu Dhabi doesn’t matter much to the three US airlines, but it is important to FedEx, which routes 44 flights through Dubai each week. -JH

EFFORTS by the Australian Customs & Border Protection Service (ACBPS) to clarify the importance of acquired work experience for a Customs broker licence are helpful to the industry – but there is a seeming disconnect on why the CBFCA’s national examination was withdrawn, writes Kelvin King.

ACBPS recently issued a notice addressing acquired experience in Customs broker licensing, by Adam Friederich, acting assistant secretary Customs and Industry Branch.

“The most important element of demonstrating acquired experience is the applicant’s employment history. While successfully completing an examination can be an additional element in demonstrating acquired experience, it is not mandatory (and) neither is it sufficient in itself,” Friederich said.

The service and the National Customs Brokers Licensing Advisory Committee (NCBLAC) still would “have regard to the completion of any national examination or assessment as one element in assessing whether or not an applicant has ‘acquired experience that fits them to be a Customs broker’”.

Both ACBPS and NCBLAC “place greater importance on the relevant work experience of the applicant. The completion of a national examination or assessment is a relevant factor when assessing the acquired experience of an applicant for a Customs broker licence. However, it is not a determinative factor.

“Completion of a national examination or assessment is not mandatory and has, in fact, never been mandatory,” he said. CBFCA’s position

Bill Murphy (left), CBFCA’s manager Professional Development and Training said last November that historically, a pass in the national examination had been accepted by ACBPS as “prima facie evidence of the acquired experience of a Customs broker licence applicant”.

This was no longer the case, as ACBP now gives more credit to an applicant’s experience, including “testimonials and documented evidence provided by the applicant and by supervising licensed Customs brokers who can attest to the experience of the applicant working in a Customs brokerage.”

By comparison, he said, “CBFCA offers a Diploma of Customs Broking which, has inherent ‘higher academic and practical demands’ with an emphasis on scenario-based learning that “simulates a workplace environment very successfully. When combined with the evidence-based process of ensuring acquired experience obtained within the actual workplace, the CBFCA believes these combined outcomes are a more than satisfactory means of determining an applicant’s suitability to be licensed as a Customs broker”.

CBFCA has stressed to the ACBP “that a process of relying heavily upon referees’ submissions to determine acquired experience needs to be rigorously enforced by the regulator as to the bona fides of these referees’ reports.

“This is important if the process is to provide confidence to industry that standards for licensing will not decline,” he said. CBFCA stands by its decision to axe the national examination and focus on the diploma, says executive director Steve Morris.

The national exam, which Morris notes was for all-comers and “not locked away for our members,” was a tough deal which sometimes saw only 18-23 per cent of students achieving its pass mark of 75 per cent, well up on the TAFE’s 50 per cent. Some people sat three to four times.

Combined with equally-rigorous testing of acquired experience, it ensured that few if any duds slipped through the system and those who passed could be proud of their achievement.

On the other hand, Morris noted, many would-be brokers began to wonder whether it was worthwhile taking this difficult pathway if Customs was putting more emphasis on acquired experience.

And it was expensive to run, partly because CBFCA was “ultra-fair” about it. If a student failed by only a little, for instance, the exam script was sent for independent reassessment.

And a warning from Bill Murphy for referees thinking of gaming the system: “False and misleading statements made in support of an employee’s application for a licence are punishable by imprisonment of up to 12 months.”

The International Air Transport Association (IATA) has released data for global air freight markets showing a 3.3 per cent increase in cargo volumes (freight tonne kilometres or FTKs) in April 2015 compared to April 2014.

However, there has been no growth in aggregated global cargo volumes since late last year.

At a regional level, only Asia-Pacific and Middle Eastern airlines reported growth in April. North American carriers reported essentially flat demand, while Europe, Latin America and Africa all reported declines when compared to 2014.

April data also revealed a slowdown from the growth for the first quarter of 2015 at an average 5.3 per cent, in line with a recent weakening in world trade growth. Despite a cyclical pick-up in the global economy, acceleration in trade and air freight demand is seen as unlikely in the near term as business confidence and export orders are flat or declining.

“After a volatile start to 2015, the market is settling down, and it is clear that momentum in air freight growth is being lost. First there is the structural challenge of world trade no longer expanding at a faster rate than domestic production. Layered on top of that trend we now see a weakening of economic indicators in the crucial air cargo markets of Asia-Pacific and Europe,” said Tony Tyler, IATA’s director general and ceo.

“These factors point toward a need to kick-start trade by reversing protectionist trade measures. Implementing the Bali Trade Facilitation Agreement would be a good start, as well as commitments to help facilitate trade in emerging markets,” said Tyler.

Also of note was the significant capacity increase of 5.5 per cent in April 2015, driving the load factor down to its lowest for the past 12 months.

Regional analysis in detail Asia-Pacific carriers reported demand growth of 4.5 per cent in April compared to April 2014, below a capacity expansion of seven per cent. Current trade volumes for emerging Asia markets are down 10 per cent, and the region has been affected by a slowdown in exports to Europe.

European carriers saw demand decline by 0.3 per cent in April, compared to a year ago while capacity grew by five per cent. Recent improvements in European business confidence have yet to be reflected in air freight volumes. A firming-up of oil prices and the Euro has meant that positive momentum from the European Central Bank stimulus has faltered.

North American airlines reported demand growth of 0.1 per cent year-on-year while capacity was cut by 1.6 per cent. A disappointing economic performance in the first quarter is expected to improve in the coming months, with the likely impact of falling oil prices and the end of the West Coast port strikes.

Middle Eastern carriers saw demand grow by 14.1 per cent on the back of increased trade within the region, along with network and capacity expansion. Capacity grew 18.5 per cent. Latin American airlines reported a fall of 6.8 per cent in demand, while capacity grew by seven per cent. Month-on-month results for carriers in the region indicate that recent declines may have come to an end. The hope is that general increases in regional trade activity start to be reflected in stronger air freight demand.

African airlines experienced a 0.2 per cent decline in demand and a 2.2 per cent decrease in capacity. The region still appears to be affected by the under-performance of the Nigerian and South African economies.

Bottom Line “After a brief optimistic period, the global outlook for cargo shows that once again the business is stagnating. But the good news is that with digital processes, new standards for pharmaceutical handling, and a focus on reducing end-to-end shipment times the air cargo industry is well-placed to stage a recovery,” said Tyler.

By Andrew Hudson, Partner, Gadens Melbourne. E: This email address is being protected from spambots. You need JavaScript enabled to view it.

Impending changes to Australia’s National Cargo Security Program (NCSP) relating to US-bound air cargo will require both the Office of Transport Security (OTS) of the Department of Infrastructure and Regional Development and affected industry to effect significant changes.

As a director of the Export Council of Australia (ECA) I have attended recent meetings of the Cargo Working Group (CWG) convened by the OTS. Clearly, many members of the ECA will be affected by these changes as will others in industry.

As many would be aware, Australia has not been subject to strict compliance with the requirement of the US TSA that all US-bound air cargo be examined at “piece level”. However that situation is shortly to expire after the TSA undertook an audit of our NCSP and recommended that 100 per cent of US-bound air cargo be examined at ‘piece level’. While the OTS continues to negotiate with the TSA to resolve the issue as soon as possible, the TSA has extended recognition until at least 31 July 2015.

At the most recent meeting of the CWG, the OTS revealed its proposed program to meet the requirements of the TSA for such ‘piece level examination’. This would require an exporter to either come within a ‘Known Consignor’ (KC) scheme or to ensure that its goods were subject to piece level examination of cargo, otherwise such cargo would not be able to be loaded. The OTS advised the CWG that the proposal was acceptable to the TSA and that it had secured Government approval to proceed with policy design and implementation. However, that does not extend to the provision of financial assistance to assist industry in managing the changes.

In the interests of providing ‘highlights’, some preliminary information is set out below:

• The new program will apply to air cargo touching on the US, whether unloaded there, or being transited through the US to be on- shipped to third countries.

• While the new program will apply to the US, the measures will be aligned with ICAO standards and meet the requirements of other areas such as the EU. The ideal would be for there to be uniform standards for all air cargo and the OTS would not object to exporters applying the program to exports to other countries.

• The aim will be for freight from KCs to be accepted without further screening by airlines as occurs elsewhere in the world. That is still subject to discussions with CTOs

• In common with Customs’ Trusted Trader Programme’ (TTP) the new scheme will address cargo security. However, the TTP does consider security in a wider context to include the entire supply chain. The OTS is working with Customs and other government agencies so that security measures in the various government ‘trusted’ programs include similar requirements so far as possible.

• The ‘regular customer’ requirements will not satisfy the requirements of the TSA and those ‘regular customers’ exporting by air to the US will need to make other arrangements.

• Membership of the KC scheme will be voluntary and subject to OTS validation and ongoing compliance oversight. OTS has indicated that the scheme will be designed to allow industry flexibility in meeting the security requirements while still satisfying the requirements of the TSA (and other jurisdictions).

• Piece level examination for those that are not KCs will be addressed in an Enhanced Air Cargo Examination (EACE) Notice to be issued by the OTS. That will set out the approved standards and methods of examination (which may include x–ray, explosive trace detection and physical examination).

Businesses providing the examination will be accredited. The current ACE notice will be amended so that cargo examined under the EACE Notice will not require additional examination at the CTO.

• Timing has yet to be finalised and subject to negotiation with the TSA. The EACE will be available to the express freight industry by 1 July 2015 and to off–site freight forwarders by 1 March 2016. The KC scheme should be open by 1 July 2016. The date for full adoption of 100 per cent piece level examination through our program has not been set although the TSA will want a firm set date that could be as early as 31 December 2016.

Clearly, there is much detail to be developed and the OTS has now embarked on an extensive process of engagement with industry including providing information as well as mapping the export process to better understand that process to allow the development of an effective program.

We do live in interesting times in the supply chain. This is taking place at the same time as Australia seeks to implement the WTO Trade Facilitation Agreement and pursue its own de – regulation agenda seeking to reduce the regulatory burden on business. However the security imperative from the TSA will always trump all those other considerations. Hopefully, Government can soften the blow by changing its position on support to business by providing financial and non-financial assistance. All businesses, especially SME exporters would be very grateful!

Businesses seeking more information about the arrangements can contact OTS via e-mail at : This email address is being protected from spambots. You need JavaScript enabled to view it. or by calling: 1800 007 024

COMPANIES that intend to use disruptive technologies will have to step outside their comfort zones and take some risks in order to reap the potential rewards, according to Australian business consultancy UXC.

UXC says success depends on minimising those risks where possible by taking a staged and carefully considered approach and working with a technology partner that understands their business, its challenges and its goals.

Cris Nicolli, managing director UXC said while disruptive IT projects carry a certain amount of risk, it is possible to reduce this risk by following eight key steps.

1. Create the business case. There are three main disruptive technology costs: Financial, time and perception and organisations must understand not all projects will run smoothly or achieve the planned outcomes.

The business must clearly articulate and analyse issues including costs and develop a strong business case for investment before taking the next step.

Innovation and disruption are unlikely to be valuable unless they are properly resourced and strategically targeted.

2. Understand and agree on the business requirements up front. Most firms implement technology in order to fulfil customer and organisational needs more effectively.

They therefore must clearly articulate the business requirements/outcomes sought before deciding on the technology to be implemented.

3. Engage key stakeholders.To bring stakeholders including employees and end users on board, they must understand how the project fits the broader business goals.

To make them fully engaged and enthusiastic about it, there needs to be clear, consistent ongoing communication including updates from the executive leadership and the project team to the rest of the stakeholders.

4. Secure executive sponsorship.Executive support is an indication that the entire company is committed to making the technology implementation work.

Without it, project teams can lose sight of the organisation’s strategic goals and failure becomes more likely.

5. Choose the right technology.While disruptive technology may look attractive, it is not necessarily the right choice. On the other hand, if a disruptive technology is the one most likely to deliver business benefits then organisations should not be dissuaded by the potential risks.

As long as the organisation has done appropriate due diligence, has a strong risk management regime in place and knows it is making the right solution, it should be well placed for success.

Choosing the right technology requires businesses to review a variety of parameters including: Depth of functionality; industry-specific features; ease of support; future development path; flexibility to adapt to the changing business model; integration with existing/future systems and scalability.

6. Future-proof the decision.By selecting a technology that maps closely to the current and future state of the business, risks are reduced. It also often is advisable to choose a solution that does not require a large amount of customisation, as this can add to ongoing running costs and future upgrade complexity. Choosing a technology that offers maximum functionality and scalability at the outset will reduce the need for constant upgrades over time. Effective organisational change management also plays a role in future-proofing the decision. 7. Demand post-implementation support.An implementation project does not end once the technology goes live. It is vital to have effective and well-resourced support in place. This will help ensure the system is fully operational, delivering value to the business and improving the productivity of those using it. 8. Implement effective governance. Corporate governance is essential for an organisation’s ongoing success and this extends to technology implementations. The greater the level of governance and scrutiny, the lower the risk of a project not succeeding. Effective governance includes the oversight of the project itself, from high level aims to detailed tactics, to ensure the project stays on track. The level and intensity of governance should be scaled to match the level of complexity of a project and the size of its investment.

DESMOND (Des) Vertannes (left) has spent more than 40 years working in air cargo. Those who know him best – and he is widely known and hugely respected in air cargo – know he strives to improve the industry. His career has included time at Air Canada, Etihad Airways and most recently, four years as head of cargo at the International Air Transport Association (IATA). He currently works as a strategic adviser at SmartKargo.

How did you come to work in air cargo? Des Vertannes: No one plans to enter the air cargo business. About 99 per cent of us fall into it by accident and I was one of those. I originally wanted to become a teacher, but as the oldest of 10 children, my father thought that earning money ‘sooner’ made more sense. I started with British European Airways (BEA) in its air cargo unit at London Heathrow, helping fill the bellies of their Tridents, BAC-111s, Viscounts and dedicated Vanguard freighters called Merchantmen – planes barely recognised today.

Let’s start with a broad view: what are the three biggest challenges air cargo faces? Security, barriers to open trade in goods and the rise in eCommerce. The first two are challenges or threats, and the last is both a threat and a remarkable opportunity.

1. The focus on security has been with us for decades, but became much sharper after 9/11 and security initiatives from government and others are ubiquitous now. What we need is a more nuanced and collaborative approach.

2. There’s not much that needs saying about tariffs and other barriers to trade in goods – most of us agree that increasing government protectionism harms world trade and hence our industry.

3. The dramatic growth of eCommerce is driven by evolving consumer behaviour. People like to buy things on line because it’s convenient, making price and feature comparisons are easy - and above all it’s fast. Universally, middle-class families are busy, and internet shopping saves time. In order to meet this growing – and to me irreversible – trend, air cargo people need to learn to adapt more quickly. Historically, we’ve not been good at change, and especially not at fast change.

How can advancing information technology help address these three challenges? I became interested in cargo IT to facilitate the fast and efficient transfer of information to all who use it. Whoever needs data should get data.

But that doesn’t happen much today. There are all kinds of blockages, some for selfish reasons that are not clearly thought out – “it’s mine” is something a three-year-old says. And even when key information does transfer between parties, it can become distorted. Sometimes governments are to blame, but often it’s the industry or the people we’ve hired to design our software and systems. Traditional air cargo IT providers see a wholesale solution, that is, airport to airport, rather than a more comprehensive and essential retail solution, from shipper to consignee. Integrators like FedEx and DHL figured this out decades ago, and it’s no wonder they’ve prospered ever since. Air cargo needs to understand this.

Another thing I learned is that developing a system in house is in most cases not the right move. Time and time again, I have seen the “make or buy” decision go in the wrong direction. The temptation to develop internally can be prompted by the best of intentions - but cost over-runs, missed deadlines and what actually is delivered can be a huge disappointment. Moreover, in my experience airlines often are delivered a system that is behind the curve in technology. It makes much more sense to contract with a proven system built for the future, not the past.

You’re a strong advocate of getting rid of paper. What’s wrong with paper? Air cargo providers move goods from point A to point B, but traditionally that also involves a whole bunch of paperwork to support each shipment. So we move the paper, and sometimes we lose the paper. And when we lose the paper, we can’t deliver the box. It’s that simple.

If we want to see what paperless can do, we need only ask our colleagues on the passenger side. The rise of e-tickets transformed distribution and lowered costs.

You’ve spoken publicly about culture change. What do you mean? It seems nearly everyone wants someone else to do the work, to make change happen.

We need leadership and we need people to take ownership. That’s the culture change. Air cargo is stuck in the old ways that no longer work.

Relationships with others in the cargo chain need to change, too. Airlines used to treat freight forwarders very paternalistically – the carriers expected forwarders to do what they were told to do. But that’s no way to treat partners, and the industry is evolving to a B2B model and procedures that treat others in the cargo chain as peers, not subordinates.

Some carriers still treat cargo as a sideline. What can be done to change that? IATA campaigned among its member airlines a few years ago to raise awareness of the value of cargo. There were three audiences: Airline ceos, government agencies (for airport investments) and the marketplace, especially investors. Among IATA member carriers, cargo averages 12 per cent of revenue, three times the average value of first class passenger business (four per cent). Yet look at all the investment in the first class product: Limousines to and from the airport, departure and arrival lounges, huge seats that turn to beds, the latest in-flight entertainment, spectacular food and wine and more. Last year, the cargo share had dropped to nine per cent and first class was still four per cent. Airlines simply do not invest what they should in cargo. Part of the reason is ‘the vicious cycle’: Low cargo revenue leads to low or no investment in IT and other items, which in turn produces disappointing revenues. It’s time to create a virtuous cycle! I also think that longer-range wide body aircraft, with ample bellies, will start to change the focus. The world is shrinking and anywhere is now one stop away. Cargo revenue will help justify the decision to buy and fly these big, long-flying planes. We’re already seeing evidence of that in North American and other carriers.

What’s your view on airlines trying to build their own cargo system? An analogy works well here: Pretend I’m pretty good with tools, and I could, with some help, build an automobile. It would run, it might even go fast enough to use on the motorway. But it would not be as good as the car I could buy from a global brand. Automobile makers invest billions in the best technology, the best safety, the best energy efficiency and styling. It works that way in cargo IT, too. Yes, you could build your own, but why wouldn’t you take products from someone who’s already done it - and done it to a very high standard. Lots of airlines have opted to build a system themselves and after millions of dollars and years of waiting have had little to show for it – and in some cases nothing.

Finally, what are the winning systems/services/products that you have access to now? I’ve advocated end-to-end solutions for years. And being 100 per cent in the cloud gives companies enormous power, for example, in making the same information visible at the same time to everyone who needs to know. SmartKargo, for example, was designed around every partner in the cargo chain, not just the carriers; Air cargo is an ecosystem, and every partner needs to be linked. That means customising tools to suit the needs of the individual, making sure systems can adapt to the particular needs of an airline.

GLOBAL freight-only giant carrier FedEx has stepped into the growing row between three US carriers and Gulf airlines Emirates, Qatar Air and Etihad (and their respective governments) and has pointed out that the three ‘foreigners’ not only carry a tidy proportion of US exports that travel by air, FedEx itself has a stake in maintaining the status quo because of its flights to and investments in the gulf region.

FedEx – which flies a fleet of 660 cargo planes across the world - has warned the US White House that any action it takes to limit foreign competitors will be seen by many as “the cold wind of US protectionism.”

And, with a major hub expansion under way in Dubai, it has stated bluntly that “we (FedEx) would potentially be subject to the greatest harm” if the United States moved against its gulf competitors.

Two other US companies with stakes in the game, United Parcel Service (UPS) and plane maker Boeing, have been coy about the case until now, but both know any changes to bilaterals would impact them severely.

While Dubai-based Emirates SkyCargo alone carries about 1000 tonnes of outbound freight a week from the USA, until now the row has been focused on the cabins, with Delta, United and American airlines claiming that the three Gulf carriers are able to offer ‘cheap’ fares to US international travellers thanks to government subsidies totalling about US$42 billion given over many years.

The three Gulf airlines have since asked for time to counter these allegations, but say any funds/benefits from their governments are only offered to them on commercial terms.

In the meantime, The US airlines had hoped the gulf carriers would freeze flights to the United States while talks between the various governments were under way, but both Qatar and Emirates continue to boost their US networks, with no halt planned. In terms of freight, Emirates SkyCargo in particular, with strong freight ties to the US, offers a compelling network of international destinations for US exporters. SkyCargo – (2014-15 financial year revenues US$3.4 billion) already serves 10 US ports using freighters and belly hold space and recently announced plans to add Orlando.

The entry of FedEx – opening the dispute to include its impact on international trade – is long overdue.

Many overseas commentators have been bemused that the Obama administration has not already dismissed the three US carriers’ complaints out of hand. Considering that only Delta and United even fly to the Gulf (and only once a day each), the vast majority of passengers and air cargo that is routed to or via Dubai (Emirates’ hub), Abu Dhabi (Etihad’s) and Doha (Qatar Air’s) have no alternative flight options other than often-longer and potentially more-expensive flights via partner carriers in Europe and Asia or Asia-Pacific.

These airline partnerships – oneworld, Star Alliance and SkyTeam – currently have more than 60 international carrier members, fly to more than 500 countries and carried more than 1.6 billion passengers last year. Some of the partner airlines including oneworld’s IAG (it has Qatar Air as its biggest shareholder) have told their US partners that they can not support a challenge to the Gulf carriers.

At home, however, FedEx already faces some carrier opposition to its stance. In a 2012 case, FedEx argued that the US government should establish a level playing field for cargo and prohibit state-owned foreign enterprises from cross-subsidising FedEx’s competitors. That case may come back to bite the freight carrier.

In the meantime, FedEx managing director has written an 11-page formal filing to the US Department of Transportation that argues against any US changes to Open Skies.

The cargo company says US airlines commonly use Open Skies agreements to build their international networks and that they eliminate competitors by working with foreign airlines. “In this case, we believe consumers (who benefit from lower fares) should be allowed to be the winners,” Sparks wrote.

Open Skies agreements with more than 100 nations allow equal access to one another’s airports without interference from the respective national governments. FedEx argues that access to the three mega-airports that have been built in Qatar, Dubai and Abu Dhabi doesn’t matter much to the three US airlines, but it is important to FedEx, which routes 44 flights through Dubai each week. -JH

EFFORTS by the Australian Customs & Border Protection Service (ACBPS) to clarify the importance of acquired work experience for a Customs broker licence are helpful to the industry – but there is a seeming disconnect on why the CBFCA’s national examination was withdrawn, writes Kelvin King.

ACBPS recently issued a notice addressing acquired experience in Customs broker licensing, by Adam Friederich, acting assistant secretary Customs and Industry Branch.

“The most important element of demonstrating acquired experience is the applicant’s employment history. While successfully completing an examination can be an additional element in demonstrating acquired experience, it is not mandatory (and) neither is it sufficient in itself,” Friederich said.

The service and the National Customs Brokers Licensing Advisory Committee (NCBLAC) still would “have regard to the completion of any national examination or assessment as one element in assessing whether or not an applicant has ‘acquired experience that fits them to be a Customs broker’”.

Both ACBPS and NCBLAC “place greater importance on the relevant work experience of the applicant. The completion of a national examination or assessment is a relevant factor when assessing the acquired experience of an applicant for a Customs broker licence. However, it is not a determinative factor.

“Completion of a national examination or assessment is not mandatory and has, in fact, never been mandatory,” he said. CBFCA’s position

Bill Murphy (left), CBFCA’s manager Professional Development and Training said last November that historically, a pass in the national examination had been accepted by ACBPS as “prima facie evidence of the acquired experience of a Customs broker licence applicant”.

This was no longer the case, as ACBP now gives more credit to an applicant’s experience, including “testimonials and documented evidence provided by the applicant and by supervising licensed Customs brokers who can attest to the experience of the applicant working in a Customs brokerage.”

By comparison, he said, “CBFCA offers a Diploma of Customs Broking which, has inherent ‘higher academic and practical demands’ with an emphasis on scenario-based learning that “simulates a workplace environment very successfully. When combined with the evidence-based process of ensuring acquired experience obtained within the actual workplace, the CBFCA believes these combined outcomes are a more than satisfactory means of determining an applicant’s suitability to be licensed as a Customs broker”.

CBFCA has stressed to the ACBP “that a process of relying heavily upon referees’ submissions to determine acquired experience needs to be rigorously enforced by the regulator as to the bona fides of these referees’ reports.

“This is important if the process is to provide confidence to industry that standards for licensing will not decline,” he said. CBFCA stands by its decision to axe the national examination and focus on the diploma, says executive director Steve Morris.

The national exam, which Morris notes was for all-comers and “not locked away for our members,” was a tough deal which sometimes saw only 18-23 per cent of students achieving its pass mark of 75 per cent, well up on the TAFE’s 50 per cent. Some people sat three to four times.

Combined with equally-rigorous testing of acquired experience, it ensured that few if any duds slipped through the system and those who passed could be proud of their achievement.

On the other hand, Morris noted, many would-be brokers began to wonder whether it was worthwhile taking this difficult pathway if Customs was putting more emphasis on acquired experience.

And it was expensive to run, partly because CBFCA was “ultra-fair” about it. If a student failed by only a little, for instance, the exam script was sent for independent reassessment.

And a warning from Bill Murphy for referees thinking of gaming the system: “False and misleading statements made in support of an employee’s application for a licence are punishable by imprisonment of up to 12 months.”

By Andrew Hudson, Partner, Gadens Melbourne. E:

By Andrew Hudson, Partner, Gadens Melbourne. E:  Cris Nicolli, managing director UXC said while disruptive IT projects carry a certain amount of risk, it is possible to reduce this risk by following eight key steps.

Cris Nicolli, managing director UXC said while disruptive IT projects carry a certain amount of risk, it is possible to reduce this risk by following eight key steps.

While Dubai-based Emirates SkyCargo alone carries about 1000 tonnes of outbound freight a week from the USA, until now the row has been focused on the cabins, with Delta, United and American airlines claiming that the three Gulf carriers are able to offer ‘cheap’ fares to US international travellers thanks to government subsidies totalling about US$42 billion given over many years.

While Dubai-based Emirates SkyCargo alone carries about 1000 tonnes of outbound freight a week from the USA, until now the row has been focused on the cabins, with Delta, United and American airlines claiming that the three Gulf carriers are able to offer ‘cheap’ fares to US international travellers thanks to government subsidies totalling about US$42 billion given over many years.  Bill Murphy (left), CBFCA’s manager Professional Development and Training said last November that historically, a pass in the national examination had been accepted by ACBPS as “prima facie evidence of the acquired experience of a Customs broker licence applicant”.

Bill Murphy (left), CBFCA’s manager Professional Development and Training said last November that historically, a pass in the national examination had been accepted by ACBPS as “prima facie evidence of the acquired experience of a Customs broker licence applicant”.