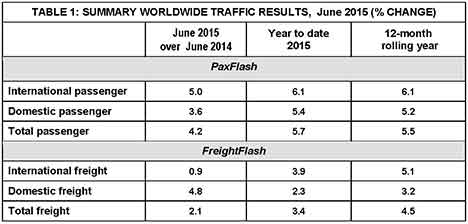

GLOBAL passenger traffic increased by 4.2 per cent year over year in June, while international and domestic traffic posted growth rates of five per cent and 3.6 per cent respectively, according to the latest data from Airports Council International (ACI). Air freight volumes showed more modest growth, at 2.1 per cent year over year. International freight experienced weakness as volumes inched up by only 0.9 per cent, whereas domestic freight traffic increased by 4.8 per cent.

Considering the economic uncertainty from the Greek debt crisis and the geopolitical risks stemming from ongoing events in Ukraine, the Middle East and West Africa, air travel has remained relatively resilient in the first half of 2015.

Accumulated passenger traffic across the world’s major airports showed growth of 5.7 per cute for the first half of 2015. The fears of a regional and global spillover effect from these events have been contained with minimal repercussions on air transport. From a regional perspective, there were no major weak spots with respect to the rise in passenger traffic for the period from January to June 2015.

Growth is likely to be around five per cent for 2015 as a whole.

Although the rate of growth in air freight markets has slowed compared to 2014, air freight has grown by 3.4 per cent for the first half of 2015 compared to the same period the previous year. Growth has become more subdued after global demand for foreign goods and commodities weakened compared to 2014. Business confidence was in limbo for the first half of 2015 and this is reflected in a weakening of orders by air and the build up of inventories. While the prospect of future global economic growth is cause for optimism, there are two forces at play which are pushing the pendulum in opposite directions. As key regional economies such as North America get back on course, a cyclical slowdown in emerging markets is dampening the potential for significant advances in the global air freight market. Thus, future growth prospects in the latter half of 2015 will remain limited.

Regional markets – Year-to-date statistics in perspective

Passengers

Africa: African air transport demand continues along on the path to recovery with modest growth of 2.3 per cent in passenger traffic for the first half of 2015. Growth prospects remain limited in the short term. Nigeria, the continent’s major oil producer and largest economy, is feeling the brunt of the drop in oil prices. Johannesburg (JNB), Africa’s busiest airport, ended the first half with 2.7 per cent gains in passenger numbers. Cairo (CAI), North Africa’s busiest airport and gateway to popular tourist destinations, saw passenger traffic jump back by 7.8 per cent in the first two quarters of 2015 as compared to the previous year.

Asia-Pacific: Asia-Pacific airports reported overall growth in passenger traffic of 8.3 per cent for the first half of the year. Despite the worries of a slowdown, both international and domestic traffic growth remain relatively strong with growth of 9.8 per cent and 7.5 per cent respectively. Beijing (PEK) grew by six per cent in the first 6 months of 2015, which is higher than year-over-year growth rates in 2014. Shanghai (PVG), the second busiest Chinese airport, posted double-digit growth of over 18 per cent over the same period. The number two ranked airport in Asia-Pacific and Japan’s busiest airport, Haneda (HND), grew by 4.8 per cent from January to June 2015 as compared to the previous year.

Europe: Regardless of the economic uncertainties that persisted in the euro area and the prospects of a Greek exit throughout 2015, the region continues to bounce back with passenger traffic rising by 4.6 per cent on a year-to-date basis. Most of the major airports that were crippled by the earlier days of the euro area crisis saw a revival in 2014. For instance, Madrid, Spain’s busiest airport which experienced a contraction in passenger numbers in 2013, recorded growth of 11.4 per cent in the first half of this year. Istanbul continues to climb the rankings among the world’s busiest airports with growth of 6.4 per cent on the year, although the growth is slowing with respect to previous years. London-Heathrow, the region’s busiest airport, posted gains of 1.3 per cent in the first half.

Latin America-Caribbean: Despite the ongoing weakness in the economies of Brazil and Argentina, the Latin American-Caribbean region has achieved growth of 5.6 per cent for the first half of 2015. The increases in traffic are largely attributed to the burgeoning domestic markets of Mexico and Colombia. Both Mexico City and Bogota experienced double-digit gains in passenger traffic of 12.4 per cent and 11.3 per cent respectively up to June 2015. On the other hand, Sao Paulo, Brazil’s busiest airport, experienced no change with respect to year-over-year growth over the same period.

Middle East: Middle East airports continue to achieve the highest growth among all regions at 8.8 per cent for the first half. Double-digit growth rates in year-over-year passenger traffic continue to be the norm for major hubs across the region. Doha and Abu Dhabi, the region’s second and third ranked airports, grew by 14.4 per cent and 17.3 per cent respectively. Dubai, the region’s busiest airport and the world’s busiest airport for international passenger traffic, grew by 10.4 per cent in the first half of 2015. The region’s airports continue to expand their capacity and capitalise on their strategic location for the transfer of passengers.

North America: Passenger numbers in North America continue to report growth above trend. Considering the maturity of the North American aviation market, growth of 4.2 per cent is coinciding with the ongoing resurgence of the United States economy. Chicago, the region’s second busiest airport, has seen its domestic traffic grow by over 10 per cent in the first half of 2015. Atlanta, the world’s busiest airport, increased by 4.4 per cent on a year-to-date basis in 2015. If the airport continues to grow at this rate for the rest of the year, it will reach the 100 million passenger mark by the end of the year.

Air freight

Africa: The African air freight market grew by 7.4 per cent in the first half of 2015. While results are mixed across the continent, JNB, a leading air freight hub, has bounced back after a bleak 2014 with respect to growth in volumes. Accumulated freight volumes from June to January 2015 grew by 11.7 per cent as compared to the same period in the previous year. CAI, the continent’s busiest air cargo hub, and JNB occupy over 30 per cent of the continent’s air freight traffic.

Asia-Pacific: A weakening of international trade activity has enfeebled the Asia-Pacific air freight market in the first half of 2016. Overall growth in volumes has slowed to three per cent on a year-to-date basis. The cross-border shipment of goods shows the weakest growth. International freight volumes, which make up the greatest proportion of freight traffic in the region, grew by only 2.7 per cent for the first six months of 2015, whereas domestic freight traffic grew by 3.8 per cent. The top global air freight hub, Hong Kong, had an increase of only 0.6 per cent in traffic for the first half of 2015. PVG and Incheon, the region’s second and third busiest air freight hubs, had year-over-year increases of five per cent and 1.5 per cent respectively.

Europe: Despite the signs of rising business confidence, the shadow of uncertainty regarding the Greek debt crisis and its potential contagion effects has left European air freight volumes in a sluggish state in the first half of 2015. Volumes inched up by 0.5 per cent during the period. The ongoing geopolitical concerns in Eastern Europe may also represent a potential obstacle on the horizon for the European air freight market. The region’s three major air freight hubs, Frankfurt, Paris and Amsterdam, experienced declines of 2.3 per cent, 4.7 per cent and 2.1 per cent respectively in the first half of 2015.

Latin America-Caribbean: With weakness in the Brazilian and Argentinian economies, growth in freight volumes in Latin-America-Caribbean has remained weak. The region saw a modest rise in freight traffic of one per cent year-over-year over the first two quarters of 2015. Growth patterns continue to be mixed for Latin America-Caribbean as a whole. While major Brazilian airports experienced declines, other airports achieved significant advances. Bogota, a Colombian airport and the region’s leading air freight hub, experienced a gain of six per cent in air freight traffic in the first half of 2015. Mexico saw a double-digit rise of 15.6 per cent in freight volumes fuelled by a burgeoning international freight market.

Middle East: With ongoing capacity expansions in the Middle East, airports and airlines have capitalised on the strategic locations of major freight hubs in the region both for long-haul and short-haul operations. The Middle East experienced the greatest increase in accumulated volumes as compared to other regions at 8.6 per cent year over year from January to June 2015. Dubai, the region’s largest freight hub, grew by 2.8 per cent over the same period. While Dubai occupies a large share of air freight traffic in the Middle East region, other airports have significantly increased volumes in the first half of 2015. Both Doha and Dubai World Central, the second and third ranked airports, grew by 11.4 per cent and 57.6 per cent respectively. With capacity for 12 million tonnes of air freight, DWC is now set to be the region’s future air cargo hub. The new airport has experienced significant growth following the commencement of operations.

North America: After the Middle East, North America posted the highest growth at 4.8 per cent year over year in the first half of 2015. The higher growth in North America continues to coincide with an American rebound. Strong economic fundamentals helped propel the air freight market. For a mature market, the relatively high level of growth in air freight volumes represents a banner year, at least with respect to the first half of 2015. Growth is exceeding 2013 levels. Although Memphis, home of FedEx, increased by only 0.6 per cent, other airports in the region achieved significant strides in year-over-year increases in volumes. With the investment in the airport’s Northeast Cargo Centre, the biggest gains were achieved by Chicago, with volumes moving up by 20.5 per cent in the first half of 2015.

AUSTRALIA and the US government have agreed ‘stringent milestones for implementation of 100 per cent piece-level examination for US-bound air cargo’, signing off formally on the tentative arrangements outlined by the Australian Federation of International Forwarders (AFIF) in late June and early July.

AFIF has been impressively proactive in sorting out what looked like being a major difficulty for Australia in meeting US deadlines.

Now a clear agreement has been reached on how the Known Consignor and Piece-Level Screening programs will progress.

Meantime, the Australian Trusted Trader pilot program is under way, as reported in our daily e-news service.

While Trusted Trader, Known Consignor and Piece-Level Screening all relate to cargo security cargo, they come under the aegis of two separate government departments.

Trusted Trader is under the control of the Department of Immigration & Border Protection which is, as we have reported on several occasions, developing it with the expert assistance of KGH Border Services, complemented by input from an industry advisory group as well as broader consultation.

Known Consignor and Piece-Level Screening are the responsibility of the Department of Infrastructure and Regional Development’s Office of Transport Security (see sidebar).

The OTS and the US Transportation Security Administration (TSA) have issued a joint statement outlining a strategy that will allow TSA to continue recognition of Australia’s National Cargo Security Program (NCSP) for US-bound air cargo until mid 2017.

Under this agreement, air carriers have 45 days from August 1 to submit a proposal for an amendment to TSA’s Standard Security Programs.

“The proposed amendments are to include aggressive timelines for meeting the current and future requirements of both governments,” explains the joint statement. “The agencies understand that the Australian government will require two years to pass appropriate legislation and develop and fully implement the framework regulations to govern a full supply chain security scheme that includes a Known Consignor scheme, consistent with the international standards established by the International Civil Aviation Organization (ICAO).

“The Australian government will introduce legislation into parliament before the end of 2015, with the regulatory requirements, rollout and full implementation of the program to be finalised no later than 30 June 2017. During the interim period as the Australian government implements its legislative and regulatory frameworks, air carriers operating to the US will establish appropriate implementation plans for their specific operations.”

It notes that providing amendments to TSA’s Standard Security Programs will “allow the contingent recognition of Australia’s NCSP while air carriers adopt a phased-in approach to the new Australian supply chain security regime while achieving compliance with US inbound requirements”.

TSA and OTS have pledged to work together and with the industry “to ensure commensurate levels of air cargo security are maintained. This agreement will ensure that bilateral trade will continue while enhancing air cargo security outcomes in both countries.”

AFIF’s chief executive Brian Lovell says the organisation believes the revised deadline of July 2017 will enable participants in the export supply chain to implement screening technology, systems and processes to ensure strict compliance with the TSA regulations and to the satisfaction of carriers operating passenger services to USA. But, he stresses, although the extension of time is a welcome outcome, the final decision regarding uplift of air cargo on a flight rests with the carrier.

AFIF has advised members to discuss specific security requirements with their respective carriers operating passenger services to USA.

Meantime, Australian Trusted Trader is moving ahead steadily. When in full operation ATT will be available to all ABN holders actively involved in the international supply chain. This includes importers, exporters, domestic and international freight companies, airports, maritime ports and brokers.

ATT aligns with WCO’s SAFE Framework, allowing more efficient clearance of low-risk cargo. Border clearance requirements are tailored to particular risks specific to a business and to their goods and supply chain.

Michaelia Cash, assistant minister for immigration and border protection, pointed out that ATT was built on the dual pillars of security and trade facilitation. “This is pioneering work as many similar programs overseas focus only on one or the other.

“The program will build resilience against organised crime groups and terrorism while simultaneously fostering active partnerships with industry and encouraging economic growth through tailored trade benefits and red tape reduction.”

What’s the OTS? — Vital to all of us it what

ALMOST everyone in the industry is familiar with the Australian Border Force – perhaps still getting use to its new name and restructuring – but there are several other government agencies with roles in air cargo which are less well known.

There’s the International Air Services Commission (IASC), for instance, which vets Australian carrier applications for authorised cargo and passenger route allocations; and the Civil Aviation Safety Authority (CASA), which ensures aviation works professionally at all levels. We report regularly on both.

While most shippers, forwarders and brokers seldom come into direct contact with IASC or CASA, one lesser known ‘agency’ – the OTS - does have a direct if not always evident impact on our daily activities.

OTS – the Office of Transport Security – is part of the Department of Infrastructure and Regional Development.

It is the government’s preventive security regulator for the aviation and maritime sectors and its primary adviser on transport security.

OTS works with Australian states and territories, other government agencies and international governments and bodies. Liaison with the transport and logistics sector is an important part of its activities.

This collaborative effort is designed to improve security and prevent transport security incidents through the gathering of intelligence, formulation of policy and as regulator, auditing compliance and ensuring a nationally-consistent approach that complies with international standards.

The agency has offices in Canberra, Brisbane, Sydney, Melbourne (with responsibility for Tasmania as well as Victoria), Adelaide, Perth and Darwin. OTS personnel are also posted in the Philippines, Thailand, UAE, Indonesia, PNG and USA.

OTS last year published Transport Security Outlook to 2025, an evidence-based view of the likely future for the transport security environment in Australia. This is available as a pdf on www.infrastructure.gov.au/transport/security

THE NEWS from the recent COAG meeting was that the Low Value Threshold (LVT) would be eliminated altogether so that, in principle, all imported goods would be subject to Customs duty and GST, writes Andrew Hudson.

Presumably it was good news for many of the Australian retailers who had lobbied for the change in the belief it would redress an unfair advantage to overseas on-line vendors as well as being good news for State Governments that hope to share in the revenue raised.

However, it is fair to say that many others are not quite as happy, because the move will add to the cost and complexity of importing goods. The total removal of the threshold would be inconsistent to overseas practice where there is at least some threshold - and it takes place at a time that the US is considering legal measures to increase its threshold to US$800, close to our LVT.

To date, very little information has been released on how the change will actually be implemented, which is not surprising given its due date of 1 July 2017. However, there are a number of practical challenges including the following:

• The 2011 Productivity Commission report into the issue included a recommendation that the low value threshold exemption for GST and duty should be reduced “where it was cost-effective to do so”. We can only assume that the Federal Government has established that the costs and complications associated with the change are outweighed by the revenue to be collected and the other intended benefits.

• Presumably the Government has satisfied itself that the reduction in the threshold does not constitute an increase in duty or the imposition of duty contrary to our FTAs.

• The reduction in duty available for goods under our FTAs will presumably still apply and those FTA also provide that no certificate or declaration of origin is required for consignments of goods below A$1,000. However, importers will still need to have evidence of the basis on which they have claimed FTA benefits. This will be a new requirement for many importers of goods in consignments worth less than A$1,000.

• The announcement did not address whether the “low value” consignments would now require completion of “Full Import Declarations” rather than “Self Assessed Clearance Declarations” or some other form of Declaration and whether that would require the use of the services of a licensed Customs broker. If Customs duty and GST is now payable, given the complexities in calculating value for duty, then Government may well require the Declaration to be produced by licensed Customs brokers.

• What sort of compliance regime will be adopted by the Department of Immigration and Border Protection for these new Declarations - or will it adopt the same approach as to all other importers that have been paying Customs duty and GST?

• Will the Integrated Cargo System be able to handle the new numbers of Declarations?

• Will the Government also require full cost recovery on the processing of the new Declarations which will attract customs duty and GST? Previously the ‘low value’ transactions did not attract the Import Processing Charge (IPC), which meant that the IPC paid by others cross-subsidised the cost to process the low value transactions. If the intent is to equalise the treatment of such low value transactions, then surely the IPC will also be charged.

• How will GST and duty be charged on overseas vendors and collected from them? Many overseas vendors are not registered for GST in Australia and being required to pay GST would be a cost that could not be recovered. One proposal is that overseas suppliers with annual Australian sales above A$75,000 would be required to register with the ATO and to collect and pay the GST to the ATO. Smaller suppliers may register with the ATO but if not, the unregistered suppliers will not pay the GST (meaning the GST would need to be assessed by Australia Post or the private cargo provider and the purchaser would need to pay the GST and a processing fee when collecting the goods). Another option would require the credit card provider or the on line sales portal to add and collect the GST at time of sale and remit the GST to the ATO.

Putting to one side the complexities, there is the fundamental question of whether the change to the practice is likely to have an impact on overseas purchases.

A recent NZ survey found that for the majority of shoppers, the addition of GST would not change shopping habits. - Andrew Hudson Partner, Gadens Melbourne. E: This email address is being protected from spambots. You need JavaScript enabled to view it.

A few operational hiccups aside, the early weeks of the Australian Border Force (ABF) have gone smoothly with officers have been sworn in, electronic systems tweaked and a fresh public face presented to the industry and public.

Fresh is a key word, given the work put into identifying and dealing with dishonest staff in the previous Customs and Border Protection agency, culling double-dippers running their own enterprises in tandem with their government jobs.

Morale, however is still a little volatile as seen in the protected industrial action undertaken by Community and Public Sector Union (CPSU) members.

A proposed enterprise agreement has been circulated to employees. Transition arrangements that maintain a range of conditions for former Customs & Border Service employees have been in place since the July 1 legal start of the new agency.

ABF’s inaugural commissioner Roman Quaedvlieg has taken an upbeat approach to his new role, saying at his swearing in that “this is the first time Australia will have a dedicated agency which will target and disrupt visa over-stayers, unscrupulous migration agents, narcotics traffickers, people smugglers and everyone in between”.

Quaedvlieg said it was an honour to “witness the beginnings of a world-class agency” and described his far-flung team as “dedicated and highly trained professionals”.

Close links with federal and state police forces will continue.

ABF is a component of the Department of Immigration and Border Protection headed by Mike Pezzullo.

The new structure’s launch came only days before the department celebrated its 70th anniversary of establishment – as the Department of Immigration – by the then prime minister Ben Chiffley. “Australia came out of World War II with the belief that we needed to increase our population to avoid the threat of invasion,” said Pezzullo.

“As many of the staff of the former Immigration Branch were still undertaking active military service, the department commenced with only 24 officers - six based in Canberra, six in Melbourne and 12 in London - and an enormous task ahead.”

ABF is running an interesting series of flashbacks on its Facebook page every Friday.

On the web: www.border.gov.au www.facebook.com/AustralianBorderForce

THE SOUTH and Central Pacific region has experienced some air route downside in the past year.

Governments have bickered over air rights, carriers searched for equipment to launch new links, while traffic – cargo and passenger – both showed volatility (although mostly veering to the positive). Infrastructure limitations in some island nations also dampened operator RoI expectations.

Recent good news among the negative and ho-hum has included a new scheduled service between Port Moresby and Port Vila, as well as the migration of a Nuku’alofa/Vava’u charter service in the Kingdom of Tonga to RPT status.

The latter could help Tonga firm up its domestic services, which have been more than a little troubled since the government sponsored Real Tonga setting up as an airline.

(Chathams Pacific withdrew as a consequence, saying competing profitable services would be an impossibility).

Real Tonga started with the China-gifted MA60 aircraft, only to give the plane back earlier this year. And it is now going to be operated by a new entity, although there is some local scepticism about the viability of this operation.

Real Tonga has since focused on smaller aircraft, hauling freight but on a small-scale basis.

It already has built on Fiji Airways/Fiji Link services to the kingdom by chartering a Link ATR 72-600 for Nuku’alofa/Vava’u flights.

Now the Fiji and Tonga governments have agreed to bump this up to regular operations. And they are talking about leveraging the relationship further.

At a MoU-signing ceremony, Aiyaz Sayed-Khaiyum, Fiji’s attorney-general and minister for civil aviation described the agreement as “an important breakthrough” that would benefit both Fiji and Tonga.

“The Tongan Government has asked Fiji Airways not only to fly domestic routes but also to examine the feasibility of operating services between Tonga and Samoa, Niue and the Cook Islands. Fiji Airways has agreed to assess the Tongan request and will make a commercial decision in the near future.” Pictured: Air Niugini crew on first flight to Port Vila

This is a realistic scenario, albeit based partly on the Kingdom of Tonga’s ongoing aviation problems.

But there have been a lot of other inter-island services mooted in the past few years, some of them by existing operators with little chance of turning big visions into reality, some by wannabe start-ups with no likelihood of success and some proposals with a strong dollop of wishful thinking.

Taking over a global transport and logistics company is a whole lot more than sending an email offering to pay mega-bucks and the target company calling back with a “yes, thanks, look forward to your e-transfer of 4.4 billion euros”.

The FedEx Corporation’s proposal to buy – through a wholly-owned subsidiary – “all of the issued and outstanding shares” in TNT Express NV is progressing slowly but seemingly with a generally positive outlook through regulatory approval channels which involve not only the EU but also Australia and New Zealand.

Both the Australian Competition & Consumer Commission (ACCC) and the NZ Commerce Commission (NZCC) have responded to FedEx’s acquisition/merger proposal by triggering the mechanism set up to give the market protection against reduction of competition and subsequent impact on pricing.

Others asked by FedEx to get the wheels of regulatory approval turning include Russia, South Korea, Brazil, China, Chile, Colombia, Israel, Japan, Turkey and Ukraine.

ACCC has formally sought submissions from interested parties - which includes competitors, sector organisations or anyone else. The deadline for e-filing is September 3.

Provisional date for a decision is October 29. This might be a final ruling (open to appeal if FedEx or any other major player is unhappy with it) or alternatively a provisional one which might show where ACCC is heading and any pitfalls it views as necessary to resolve. In its request for submissions – sent to those identified as interested parties with a welcome to pass it on to others if wished – ACCC asked for advice on various scenarios as well as the general provisos of a competitiveness investigation.

One asks submitters: “Do you consider that the merged entity would have an increased ability to increase prices or reduce service levels to customers in Australia or would it be prevented from doing so by competition from DHL, UPS and others?”

And, it requests, “please address the potential for (i) Australia Post (including Star Track Express); (ii) Toll; and (iii) freight forwarders generally (for example, of shipments over 50kg), to be effective competitors to the merged entity in relation to supply of express international small package delivery services to customers in Australia”.

It also asks submitters to “identify any relevant barriers to expansion by existing providers of express international small package delivery services in Australia, or entry by new providers. “Do you consider it likely that existing competitors would expand and/or new competitors would enter if the merged FedEx/TNT increased prices or reduced service levels?

“Would you expect the proposed acquisition to increase these barriers to entry/expansion?”

Submissions are confidential to the extent that they are neither published nor disclosed to a third party other than ACCC advisers or consultants. But they can be made public in certain circumstances when compelled by law; ACCC is then required to advise the submitter/s so they have an opportunity to be heard.

NZCC has asked even more detailed questions of submitters as it undertakes its investigation.

Its aim is to have a decision ready by September 25 but warns this might be extended depending on how the investigation progresses.

In Europe, things also are moving along. The EC has initiated a ‘phase II review’ which calls for more information – this is the next step in the process where the European Commission conducts an in-depth analysis under the EU Merger Regulation before coming to a decision.

David Binks, president of FedEx Express Europe, said the group was confident the combination would increase competition and create benefits for customers.

“We continue to make progress on all of the necessary regulatory steps around the world that would allow us to complete this transaction in the first half of 2016 and unite two great teams that share a passion for customer service.”

TNT Express shareholders are to consider the FedEx offer on October 5. They have until October 30 for a decision.

There is solid support for the deal from TNT directors, major shareholders, staff councils and unions.

B763 freighters to come FedEx is the throes of a substantial fleet renewal program.

In June the group announced it had permanently retired 15 aircraft and 21 related engines. These include seven MD11, three A300, four A310 and one MD10-10 freighters.

An industry advisory from FedEx pointed out that “the B767 provides similar capacity as the MD10 with improved reliability, an approximate 30 per cent increase in fuel efficiency and a minimum of a 20 per cent reduction in unit operating costs”.

The company confirmed this B767 enthusiasm in late July (as reported in our daily e-news) when it announced an order for a further 50 B763 freighters, taking its total firm orders of the type to 106. It also holds options for a further 50 B763F.

FedEx president and ceo David Bronczek said “acquiring additional 767F aircraft is a continuation of our very successful air fleet modernisation program and will enable us to reduce structural costs, improve our fuel efficiency and enhance the reliability of our global network”.

For Boeing, the late-July order and options have breathed new life into the B767 production line.

GLOBAL passenger traffic increased by 4.2 per cent year over year in June, while international and domestic traffic posted growth rates of five per cent and 3.6 per cent respectively, according to the latest data from Airports Council International (ACI). Air freight volumes showed more modest growth, at 2.1 per cent year over year. International freight experienced weakness as volumes inched up by only 0.9 per cent, whereas domestic freight traffic increased by 4.8 per cent.

Considering the economic uncertainty from the Greek debt crisis and the geopolitical risks stemming from ongoing events in Ukraine, the Middle East and West Africa, air travel has remained relatively resilient in the first half of 2015.

Accumulated passenger traffic across the world’s major airports showed growth of 5.7 per cute for the first half of 2015. The fears of a regional and global spillover effect from these events have been contained with minimal repercussions on air transport. From a regional perspective, there were no major weak spots with respect to the rise in passenger traffic for the period from January to June 2015.

Growth is likely to be around five per cent for 2015 as a whole.

Although the rate of growth in air freight markets has slowed compared to 2014, air freight has grown by 3.4 per cent for the first half of 2015 compared to the same period the previous year. Growth has become more subdued after global demand for foreign goods and commodities weakened compared to 2014. Business confidence was in limbo for the first half of 2015 and this is reflected in a weakening of orders by air and the build up of inventories. While the prospect of future global economic growth is cause for optimism, there are two forces at play which are pushing the pendulum in opposite directions. As key regional economies such as North America get back on course, a cyclical slowdown in emerging markets is dampening the potential for significant advances in the global air freight market. Thus, future growth prospects in the latter half of 2015 will remain limited.

Regional markets – Year-to-date statistics in perspective

Passengers

Africa: African air transport demand continues along on the path to recovery with modest growth of 2.3 per cent in passenger traffic for the first half of 2015. Growth prospects remain limited in the short term. Nigeria, the continent’s major oil producer and largest economy, is feeling the brunt of the drop in oil prices. Johannesburg (JNB), Africa’s busiest airport, ended the first half with 2.7 per cent gains in passenger numbers. Cairo (CAI), North Africa’s busiest airport and gateway to popular tourist destinations, saw passenger traffic jump back by 7.8 per cent in the first two quarters of 2015 as compared to the previous year.

Asia-Pacific: Asia-Pacific airports reported overall growth in passenger traffic of 8.3 per cent for the first half of the year. Despite the worries of a slowdown, both international and domestic traffic growth remain relatively strong with growth of 9.8 per cent and 7.5 per cent respectively. Beijing (PEK) grew by six per cent in the first 6 months of 2015, which is higher than year-over-year growth rates in 2014. Shanghai (PVG), the second busiest Chinese airport, posted double-digit growth of over 18 per cent over the same period. The number two ranked airport in Asia-Pacific and Japan’s busiest airport, Haneda (HND), grew by 4.8 per cent from January to June 2015 as compared to the previous year.

Europe: Regardless of the economic uncertainties that persisted in the euro area and the prospects of a Greek exit throughout 2015, the region continues to bounce back with passenger traffic rising by 4.6 per cent on a year-to-date basis. Most of the major airports that were crippled by the earlier days of the euro area crisis saw a revival in 2014. For instance, Madrid, Spain’s busiest airport which experienced a contraction in passenger numbers in 2013, recorded growth of 11.4 per cent in the first half of this year. Istanbul continues to climb the rankings among the world’s busiest airports with growth of 6.4 per cent on the year, although the growth is slowing with respect to previous years. London-Heathrow, the region’s busiest airport, posted gains of 1.3 per cent in the first half.

Latin America-Caribbean: Despite the ongoing weakness in the economies of Brazil and Argentina, the Latin American-Caribbean region has achieved growth of 5.6 per cent for the first half of 2015. The increases in traffic are largely attributed to the burgeoning domestic markets of Mexico and Colombia. Both Mexico City and Bogota experienced double-digit gains in passenger traffic of 12.4 per cent and 11.3 per cent respectively up to June 2015. On the other hand, Sao Paulo, Brazil’s busiest airport, experienced no change with respect to year-over-year growth over the same period.

Middle East: Middle East airports continue to achieve the highest growth among all regions at 8.8 per cent for the first half. Double-digit growth rates in year-over-year passenger traffic continue to be the norm for major hubs across the region. Doha and Abu Dhabi, the region’s second and third ranked airports, grew by 14.4 per cent and 17.3 per cent respectively. Dubai, the region’s busiest airport and the world’s busiest airport for international passenger traffic, grew by 10.4 per cent in the first half of 2015. The region’s airports continue to expand their capacity and capitalise on their strategic location for the transfer of passengers.

North America: Passenger numbers in North America continue to report growth above trend. Considering the maturity of the North American aviation market, growth of 4.2 per cent is coinciding with the ongoing resurgence of the United States economy. Chicago, the region’s second busiest airport, has seen its domestic traffic grow by over 10 per cent in the first half of 2015. Atlanta, the world’s busiest airport, increased by 4.4 per cent on a year-to-date basis in 2015. If the airport continues to grow at this rate for the rest of the year, it will reach the 100 million passenger mark by the end of the year.

Air freight

Africa: The African air freight market grew by 7.4 per cent in the first half of 2015. While results are mixed across the continent, JNB, a leading air freight hub, has bounced back after a bleak 2014 with respect to growth in volumes. Accumulated freight volumes from June to January 2015 grew by 11.7 per cent as compared to the same period in the previous year. CAI, the continent’s busiest air cargo hub, and JNB occupy over 30 per cent of the continent’s air freight traffic.

Asia-Pacific: A weakening of international trade activity has enfeebled the Asia-Pacific air freight market in the first half of 2016. Overall growth in volumes has slowed to three per cent on a year-to-date basis. The cross-border shipment of goods shows the weakest growth. International freight volumes, which make up the greatest proportion of freight traffic in the region, grew by only 2.7 per cent for the first six months of 2015, whereas domestic freight traffic grew by 3.8 per cent. The top global air freight hub, Hong Kong, had an increase of only 0.6 per cent in traffic for the first half of 2015. PVG and Incheon, the region’s second and third busiest air freight hubs, had year-over-year increases of five per cent and 1.5 per cent respectively.

Europe: Despite the signs of rising business confidence, the shadow of uncertainty regarding the Greek debt crisis and its potential contagion effects has left European air freight volumes in a sluggish state in the first half of 2015. Volumes inched up by 0.5 per cent during the period. The ongoing geopolitical concerns in Eastern Europe may also represent a potential obstacle on the horizon for the European air freight market. The region’s three major air freight hubs, Frankfurt, Paris and Amsterdam, experienced declines of 2.3 per cent, 4.7 per cent and 2.1 per cent respectively in the first half of 2015.

Latin America-Caribbean: With weakness in the Brazilian and Argentinian economies, growth in freight volumes in Latin-America-Caribbean has remained weak. The region saw a modest rise in freight traffic of one per cent year-over-year over the first two quarters of 2015. Growth patterns continue to be mixed for Latin America-Caribbean as a whole. While major Brazilian airports experienced declines, other airports achieved significant advances. Bogota, a Colombian airport and the region’s leading air freight hub, experienced a gain of six per cent in air freight traffic in the first half of 2015. Mexico saw a double-digit rise of 15.6 per cent in freight volumes fuelled by a burgeoning international freight market.

Middle East: With ongoing capacity expansions in the Middle East, airports and airlines have capitalised on the strategic locations of major freight hubs in the region both for long-haul and short-haul operations. The Middle East experienced the greatest increase in accumulated volumes as compared to other regions at 8.6 per cent year over year from January to June 2015. Dubai, the region’s largest freight hub, grew by 2.8 per cent over the same period. While Dubai occupies a large share of air freight traffic in the Middle East region, other airports have significantly increased volumes in the first half of 2015. Both Doha and Dubai World Central, the second and third ranked airports, grew by 11.4 per cent and 57.6 per cent respectively. With capacity for 12 million tonnes of air freight, DWC is now set to be the region’s future air cargo hub. The new airport has experienced significant growth following the commencement of operations.

North America: After the Middle East, North America posted the highest growth at 4.8 per cent year over year in the first half of 2015. The higher growth in North America continues to coincide with an American rebound. Strong economic fundamentals helped propel the air freight market. For a mature market, the relatively high level of growth in air freight volumes represents a banner year, at least with respect to the first half of 2015. Growth is exceeding 2013 levels. Although Memphis, home of FedEx, increased by only 0.6 per cent, other airports in the region achieved significant strides in year-over-year increases in volumes. With the investment in the airport’s Northeast Cargo Centre, the biggest gains were achieved by Chicago, with volumes moving up by 20.5 per cent in the first half of 2015.

AUSTRALIA and the US government have agreed ‘stringent milestones for implementation of 100 per cent piece-level examination for US-bound air cargo’, signing off formally on the tentative arrangements outlined by the Australian Federation of International Forwarders (AFIF) in late June and early July.

AFIF has been impressively proactive in sorting out what looked like being a major difficulty for Australia in meeting US deadlines.

Now a clear agreement has been reached on how the Known Consignor and Piece-Level Screening programs will progress.

Meantime, the Australian Trusted Trader pilot program is under way, as reported in our daily e-news service.

While Trusted Trader, Known Consignor and Piece-Level Screening all relate to cargo security cargo, they come under the aegis of two separate government departments.

Trusted Trader is under the control of the Department of Immigration & Border Protection which is, as we have reported on several occasions, developing it with the expert assistance of KGH Border Services, complemented by input from an industry advisory group as well as broader consultation.

Known Consignor and Piece-Level Screening are the responsibility of the Department of Infrastructure and Regional Development’s Office of Transport Security (see sidebar).

The OTS and the US Transportation Security Administration (TSA) have issued a joint statement outlining a strategy that will allow TSA to continue recognition of Australia’s National Cargo Security Program (NCSP) for US-bound air cargo until mid 2017.

Under this agreement, air carriers have 45 days from August 1 to submit a proposal for an amendment to TSA’s Standard Security Programs.

“The proposed amendments are to include aggressive timelines for meeting the current and future requirements of both governments,” explains the joint statement. “The agencies understand that the Australian government will require two years to pass appropriate legislation and develop and fully implement the framework regulations to govern a full supply chain security scheme that includes a Known Consignor scheme, consistent with the international standards established by the International Civil Aviation Organization (ICAO).

“The Australian government will introduce legislation into parliament before the end of 2015, with the regulatory requirements, rollout and full implementation of the program to be finalised no later than 30 June 2017. During the interim period as the Australian government implements its legislative and regulatory frameworks, air carriers operating to the US will establish appropriate implementation plans for their specific operations.”

It notes that providing amendments to TSA’s Standard Security Programs will “allow the contingent recognition of Australia’s NCSP while air carriers adopt a phased-in approach to the new Australian supply chain security regime while achieving compliance with US inbound requirements”.

TSA and OTS have pledged to work together and with the industry “to ensure commensurate levels of air cargo security are maintained. This agreement will ensure that bilateral trade will continue while enhancing air cargo security outcomes in both countries.”

AFIF’s chief executive Brian Lovell says the organisation believes the revised deadline of July 2017 will enable participants in the export supply chain to implement screening technology, systems and processes to ensure strict compliance with the TSA regulations and to the satisfaction of carriers operating passenger services to USA. But, he stresses, although the extension of time is a welcome outcome, the final decision regarding uplift of air cargo on a flight rests with the carrier.

AFIF has advised members to discuss specific security requirements with their respective carriers operating passenger services to USA.

Meantime, Australian Trusted Trader is moving ahead steadily. When in full operation ATT will be available to all ABN holders actively involved in the international supply chain. This includes importers, exporters, domestic and international freight companies, airports, maritime ports and brokers.

ATT aligns with WCO’s SAFE Framework, allowing more efficient clearance of low-risk cargo. Border clearance requirements are tailored to particular risks specific to a business and to their goods and supply chain.

Michaelia Cash, assistant minister for immigration and border protection, pointed out that ATT was built on the dual pillars of security and trade facilitation. “This is pioneering work as many similar programs overseas focus only on one or the other.

“The program will build resilience against organised crime groups and terrorism while simultaneously fostering active partnerships with industry and encouraging economic growth through tailored trade benefits and red tape reduction.”

What’s the OTS? — Vital to all of us it what

ALMOST everyone in the industry is familiar with the Australian Border Force – perhaps still getting use to its new name and restructuring – but there are several other government agencies with roles in air cargo which are less well known.

There’s the International Air Services Commission (IASC), for instance, which vets Australian carrier applications for authorised cargo and passenger route allocations; and the Civil Aviation Safety Authority (CASA), which ensures aviation works professionally at all levels. We report regularly on both.

While most shippers, forwarders and brokers seldom come into direct contact with IASC or CASA, one lesser known ‘agency’ – the OTS - does have a direct if not always evident impact on our daily activities.

OTS – the Office of Transport Security – is part of the Department of Infrastructure and Regional Development.

It is the government’s preventive security regulator for the aviation and maritime sectors and its primary adviser on transport security.

OTS works with Australian states and territories, other government agencies and international governments and bodies. Liaison with the transport and logistics sector is an important part of its activities.

This collaborative effort is designed to improve security and prevent transport security incidents through the gathering of intelligence, formulation of policy and as regulator, auditing compliance and ensuring a nationally-consistent approach that complies with international standards.

The agency has offices in Canberra, Brisbane, Sydney, Melbourne (with responsibility for Tasmania as well as Victoria), Adelaide, Perth and Darwin. OTS personnel are also posted in the Philippines, Thailand, UAE, Indonesia, PNG and USA.

OTS last year published Transport Security Outlook to 2025, an evidence-based view of the likely future for the transport security environment in Australia. This is available as a pdf on www.infrastructure.gov.au/transport/security

THE NEWS from the recent COAG meeting was that the Low Value Threshold (LVT) would be eliminated altogether so that, in principle, all imported goods would be subject to Customs duty and GST, writes Andrew Hudson.

Presumably it was good news for many of the Australian retailers who had lobbied for the change in the belief it would redress an unfair advantage to overseas on-line vendors as well as being good news for State Governments that hope to share in the revenue raised.

However, it is fair to say that many others are not quite as happy, because the move will add to the cost and complexity of importing goods. The total removal of the threshold would be inconsistent to overseas practice where there is at least some threshold - and it takes place at a time that the US is considering legal measures to increase its threshold to US$800, close to our LVT.

To date, very little information has been released on how the change will actually be implemented, which is not surprising given its due date of 1 July 2017. However, there are a number of practical challenges including the following:

• The 2011 Productivity Commission report into the issue included a recommendation that the low value threshold exemption for GST and duty should be reduced “where it was cost-effective to do so”. We can only assume that the Federal Government has established that the costs and complications associated with the change are outweighed by the revenue to be collected and the other intended benefits.

• Presumably the Government has satisfied itself that the reduction in the threshold does not constitute an increase in duty or the imposition of duty contrary to our FTAs.

• The reduction in duty available for goods under our FTAs will presumably still apply and those FTA also provide that no certificate or declaration of origin is required for consignments of goods below A$1,000. However, importers will still need to have evidence of the basis on which they have claimed FTA benefits. This will be a new requirement for many importers of goods in consignments worth less than A$1,000.

• The announcement did not address whether the “low value” consignments would now require completion of “Full Import Declarations” rather than “Self Assessed Clearance Declarations” or some other form of Declaration and whether that would require the use of the services of a licensed Customs broker. If Customs duty and GST is now payable, given the complexities in calculating value for duty, then Government may well require the Declaration to be produced by licensed Customs brokers.

• What sort of compliance regime will be adopted by the Department of Immigration and Border Protection for these new Declarations - or will it adopt the same approach as to all other importers that have been paying Customs duty and GST?

• Will the Integrated Cargo System be able to handle the new numbers of Declarations?

• Will the Government also require full cost recovery on the processing of the new Declarations which will attract customs duty and GST? Previously the ‘low value’ transactions did not attract the Import Processing Charge (IPC), which meant that the IPC paid by others cross-subsidised the cost to process the low value transactions. If the intent is to equalise the treatment of such low value transactions, then surely the IPC will also be charged.

• How will GST and duty be charged on overseas vendors and collected from them? Many overseas vendors are not registered for GST in Australia and being required to pay GST would be a cost that could not be recovered. One proposal is that overseas suppliers with annual Australian sales above A$75,000 would be required to register with the ATO and to collect and pay the GST to the ATO. Smaller suppliers may register with the ATO but if not, the unregistered suppliers will not pay the GST (meaning the GST would need to be assessed by Australia Post or the private cargo provider and the purchaser would need to pay the GST and a processing fee when collecting the goods). Another option would require the credit card provider or the on line sales portal to add and collect the GST at time of sale and remit the GST to the ATO.

Putting to one side the complexities, there is the fundamental question of whether the change to the practice is likely to have an impact on overseas purchases.

A recent NZ survey found that for the majority of shoppers, the addition of GST would not change shopping habits. - Andrew Hudson Partner, Gadens Melbourne. E: This email address is being protected from spambots. You need JavaScript enabled to view it.

A few operational hiccups aside, the early weeks of the Australian Border Force (ABF) have gone smoothly with officers have been sworn in, electronic systems tweaked and a fresh public face presented to the industry and public.

Fresh is a key word, given the work put into identifying and dealing with dishonest staff in the previous Customs and Border Protection agency, culling double-dippers running their own enterprises in tandem with their government jobs.

Morale, however is still a little volatile as seen in the protected industrial action undertaken by Community and Public Sector Union (CPSU) members.

A proposed enterprise agreement has been circulated to employees. Transition arrangements that maintain a range of conditions for former Customs & Border Service employees have been in place since the July 1 legal start of the new agency.

ABF’s inaugural commissioner Roman Quaedvlieg has taken an upbeat approach to his new role, saying at his swearing in that “this is the first time Australia will have a dedicated agency which will target and disrupt visa over-stayers, unscrupulous migration agents, narcotics traffickers, people smugglers and everyone in between”.

Quaedvlieg said it was an honour to “witness the beginnings of a world-class agency” and described his far-flung team as “dedicated and highly trained professionals”.

Close links with federal and state police forces will continue.

ABF is a component of the Department of Immigration and Border Protection headed by Mike Pezzullo.

The new structure’s launch came only days before the department celebrated its 70th anniversary of establishment – as the Department of Immigration – by the then prime minister Ben Chiffley. “Australia came out of World War II with the belief that we needed to increase our population to avoid the threat of invasion,” said Pezzullo.

“As many of the staff of the former Immigration Branch were still undertaking active military service, the department commenced with only 24 officers - six based in Canberra, six in Melbourne and 12 in London - and an enormous task ahead.”

ABF is running an interesting series of flashbacks on its Facebook page every Friday.

On the web: www.border.gov.au www.facebook.com/AustralianBorderForce

THE SOUTH and Central Pacific region has experienced some air route downside in the past year.

Governments have bickered over air rights, carriers searched for equipment to launch new links, while traffic – cargo and passenger – both showed volatility (although mostly veering to the positive). Infrastructure limitations in some island nations also dampened operator RoI expectations.

Recent good news among the negative and ho-hum has included a new scheduled service between Port Moresby and Port Vila, as well as the migration of a Nuku’alofa/Vava’u charter service in the Kingdom of Tonga to RPT status.

The latter could help Tonga firm up its domestic services, which have been more than a little troubled since the government sponsored Real Tonga setting up as an airline.

(Chathams Pacific withdrew as a consequence, saying competing profitable services would be an impossibility).

Real Tonga started with the China-gifted MA60 aircraft, only to give the plane back earlier this year. And it is now going to be operated by a new entity, although there is some local scepticism about the viability of this operation.

Real Tonga has since focused on smaller aircraft, hauling freight but on a small-scale basis.

It already has built on Fiji Airways/Fiji Link services to the kingdom by chartering a Link ATR 72-600 for Nuku’alofa/Vava’u flights.

Now the Fiji and Tonga governments have agreed to bump this up to regular operations. And they are talking about leveraging the relationship further.

At a MoU-signing ceremony, Aiyaz Sayed-Khaiyum, Fiji’s attorney-general and minister for civil aviation described the agreement as “an important breakthrough” that would benefit both Fiji and Tonga.

“The Tongan Government has asked Fiji Airways not only to fly domestic routes but also to examine the feasibility of operating services between Tonga and Samoa, Niue and the Cook Islands. Fiji Airways has agreed to assess the Tongan request and will make a commercial decision in the near future.” Pictured: Air Niugini crew on first flight to Port Vila

This is a realistic scenario, albeit based partly on the Kingdom of Tonga’s ongoing aviation problems.

But there have been a lot of other inter-island services mooted in the past few years, some of them by existing operators with little chance of turning big visions into reality, some by wannabe start-ups with no likelihood of success and some proposals with a strong dollop of wishful thinking.

Taking over a global transport and logistics company is a whole lot more than sending an email offering to pay mega-bucks and the target company calling back with a “yes, thanks, look forward to your e-transfer of 4.4 billion euros”.

The FedEx Corporation’s proposal to buy – through a wholly-owned subsidiary – “all of the issued and outstanding shares” in TNT Express NV is progressing slowly but seemingly with a generally positive outlook through regulatory approval channels which involve not only the EU but also Australia and New Zealand.

Both the Australian Competition & Consumer Commission (ACCC) and the NZ Commerce Commission (NZCC) have responded to FedEx’s acquisition/merger proposal by triggering the mechanism set up to give the market protection against reduction of competition and subsequent impact on pricing.

Others asked by FedEx to get the wheels of regulatory approval turning include Russia, South Korea, Brazil, China, Chile, Colombia, Israel, Japan, Turkey and Ukraine.

ACCC has formally sought submissions from interested parties - which includes competitors, sector organisations or anyone else. The deadline for e-filing is September 3.

Provisional date for a decision is October 29. This might be a final ruling (open to appeal if FedEx or any other major player is unhappy with it) or alternatively a provisional one which might show where ACCC is heading and any pitfalls it views as necessary to resolve. In its request for submissions – sent to those identified as interested parties with a welcome to pass it on to others if wished – ACCC asked for advice on various scenarios as well as the general provisos of a competitiveness investigation.

One asks submitters: “Do you consider that the merged entity would have an increased ability to increase prices or reduce service levels to customers in Australia or would it be prevented from doing so by competition from DHL, UPS and others?”

And, it requests, “please address the potential for (i) Australia Post (including Star Track Express); (ii) Toll; and (iii) freight forwarders generally (for example, of shipments over 50kg), to be effective competitors to the merged entity in relation to supply of express international small package delivery services to customers in Australia”.

It also asks submitters to “identify any relevant barriers to expansion by existing providers of express international small package delivery services in Australia, or entry by new providers. “Do you consider it likely that existing competitors would expand and/or new competitors would enter if the merged FedEx/TNT increased prices or reduced service levels?

“Would you expect the proposed acquisition to increase these barriers to entry/expansion?”

Submissions are confidential to the extent that they are neither published nor disclosed to a third party other than ACCC advisers or consultants. But they can be made public in certain circumstances when compelled by law; ACCC is then required to advise the submitter/s so they have an opportunity to be heard.

NZCC has asked even more detailed questions of submitters as it undertakes its investigation.

Its aim is to have a decision ready by September 25 but warns this might be extended depending on how the investigation progresses.

In Europe, things also are moving along. The EC has initiated a ‘phase II review’ which calls for more information – this is the next step in the process where the European Commission conducts an in-depth analysis under the EU Merger Regulation before coming to a decision.

David Binks, president of FedEx Express Europe, said the group was confident the combination would increase competition and create benefits for customers.

“We continue to make progress on all of the necessary regulatory steps around the world that would allow us to complete this transaction in the first half of 2016 and unite two great teams that share a passion for customer service.”

TNT Express shareholders are to consider the FedEx offer on October 5. They have until October 30 for a decision.

There is solid support for the deal from TNT directors, major shareholders, staff councils and unions.

B763 freighters to come FedEx is the throes of a substantial fleet renewal program.

In June the group announced it had permanently retired 15 aircraft and 21 related engines. These include seven MD11, three A300, four A310 and one MD10-10 freighters.

An industry advisory from FedEx pointed out that “the B767 provides similar capacity as the MD10 with improved reliability, an approximate 30 per cent increase in fuel efficiency and a minimum of a 20 per cent reduction in unit operating costs”.

The company confirmed this B767 enthusiasm in late July (as reported in our daily e-news) when it announced an order for a further 50 B763 freighters, taking its total firm orders of the type to 106. It also holds options for a further 50 B763F.

FedEx president and ceo David Bronczek said “acquiring additional 767F aircraft is a continuation of our very successful air fleet modernisation program and will enable us to reduce structural costs, improve our fuel efficiency and enhance the reliability of our global network”.

For Boeing, the late-July order and options have breathed new life into the B767 production line.

Although the rate of growth in air freight markets has slowed compared to 2014, air freight has grown by 3.4 per cent for the first half of 2015 compared to the same period the previous year. Growth has become more subdued after global demand for foreign goods and commodities weakened compared to 2014. Business confidence was in limbo for the first half of 2015 and this is reflected in a weakening of orders by air and the build up of inventories. While the prospect of future global economic growth is cause for optimism, there are two forces at play which are pushing the pendulum in opposite directions. As key regional economies such as North America get back on course, a cyclical slowdown in emerging markets is dampening the potential for significant advances in the global air freight market. Thus, future growth prospects in the latter half of 2015 will remain limited.

Although the rate of growth in air freight markets has slowed compared to 2014, air freight has grown by 3.4 per cent for the first half of 2015 compared to the same period the previous year. Growth has become more subdued after global demand for foreign goods and commodities weakened compared to 2014. Business confidence was in limbo for the first half of 2015 and this is reflected in a weakening of orders by air and the build up of inventories. While the prospect of future global economic growth is cause for optimism, there are two forces at play which are pushing the pendulum in opposite directions. As key regional economies such as North America get back on course, a cyclical slowdown in emerging markets is dampening the potential for significant advances in the global air freight market. Thus, future growth prospects in the latter half of 2015 will remain limited. Latin America-Caribbean:

Latin America-Caribbean:  urity Administration (TSA) have issued a joint statement outlining a strategy that will allow TSA to continue recognition of Australia’s National Cargo Security Program (NCSP) for US-bound air cargo until mid 2017.

urity Administration (TSA) have issued a joint statement outlining a strategy that will allow TSA to continue recognition of Australia’s National Cargo Security Program (NCSP) for US-bound air cargo until mid 2017.

ng the following:

ng the following: ABF’s inaugural commissioner Roman Quaedvlieg has taken an upbeat approach to his new role, saying at his swearing in that “this is the first time Australia will have a dedicated agency which will target and disrupt visa over-stayers, unscrupulous migration agents, narcotics traffickers, people smugglers and everyone in between”.

ABF’s inaugural commissioner Roman Quaedvlieg has taken an upbeat approach to his new role, saying at his swearing in that “this is the first time Australia will have a dedicated agency which will target and disrupt visa over-stayers, unscrupulous migration agents, narcotics traffickers, people smugglers and everyone in between”. The latter could help Tonga firm up its domestic services, which have been more than a little troubled since the government sponsored Real Tonga setting up as an airline.

The latter could help Tonga firm up its domestic services, which have been more than a little troubled since the government sponsored Real Tonga setting up as an airline.

um of a 20 per cent reduction in unit operating costs”.

um of a 20 per cent reduction in unit operating costs”.